Social inflation refers to the increase in the cost of insurance claims, specifically liability claims, that exceeds the rate of general economic inflation. This means that the cost of settling claims is rising faster than the overall increase in prices within the economy. Social inflation is driven by various societal and behavioral trends, including a growing tendency to file lawsuits, increased jury awards, and evolving perceptions of liability and risk.

Economic inflation has been largely benign until the aftermath of COVID related spending, supply chain issues, and the Russian-Ukraine 'special military operation'. As a result, up till now, few appreciated Insureware's emphasis on the importance of measuring inflation, especially social inflation. Now, every insurance company is on high alert for how inflation is affecting their business, pricing models, and risk capital requirements.

Economic inflation is generally quantified by economists employed by public or private institutions and the figures published reflect a variety of stakeholder priorities which will not apply to every kind of situation. Social inflation estimates where they are published tend to be narrowly focused on particular tranches of the economy. This may be helpful in some sectors but cannot substitute for a direct measurement of actual inflation for a specific line of business. Where this can be computed it must be done after carefully separating out the effects of development and changing exposure.

EY USA uses ICRFS's PTF modeling framework to measure inflation

EY USA (an Insureware client since 1996) gave a CAS Webinar: Social Inflation and Emerging Mass Torts – Now, Next and Beyond | Casualty Actuarial Society (pathlms.com)) on social inflation in March. If you click on the link and then Resources you can view the PDF.

The webinar refers to the Probabilistic Trend Family (PTF) modeling framework as ICRFS is used to model inflation trends.

Insureware's PTF modeling framework and quantifying social inflation trends

In the Probabilistic Trend Family (PTF) modeling framework, we identify a parsimonious model describing the trends in the three directions (development, accident, and calendar), along with the volatility about the trend structure. The importance here is the measurement of trends in the calendar direction.

PTF differs from other actuarial solutions in two key ways. Firstly, a PTF model is not pre-defined but rather is tailored to each company’s data. This enables the tool to extract the salient statistical features of any loss development array and produce meaningful results for all aspects of the liability distributions. Any modeling assumptions can be tested and verified that they are supported by the data. Secondly, PTF allows for parameters in the calendar direction. Other methods do not parametise the calendar direction meaning that the calendar effects are picked up in either the development or accident direction - neither effectively or with any quantification.

Link ratio methods overstate social inflation: projections are too high

Consider anonymized Paid Loss data for an Auto Insurance provider (segment: Bodily Injury).

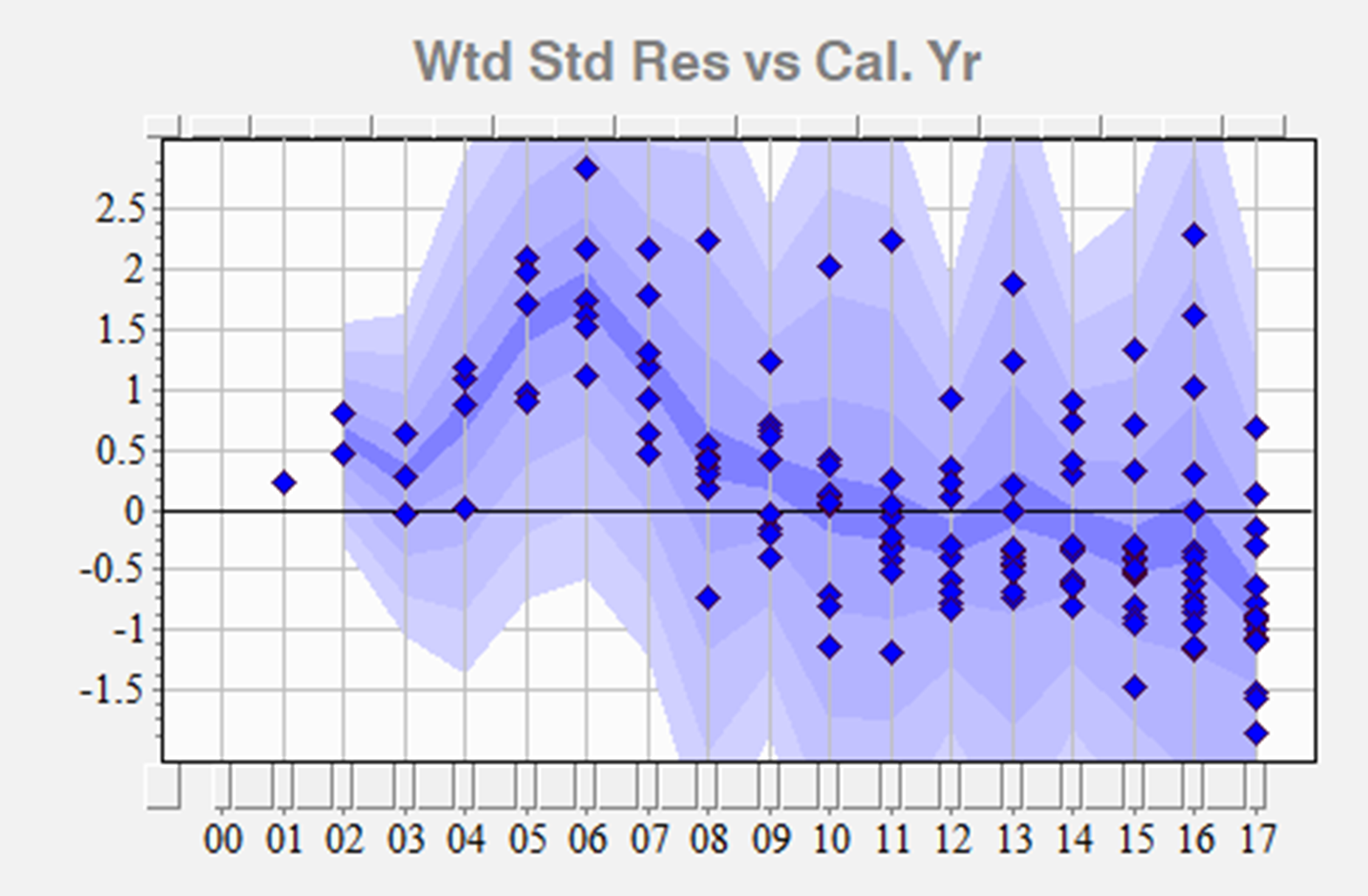

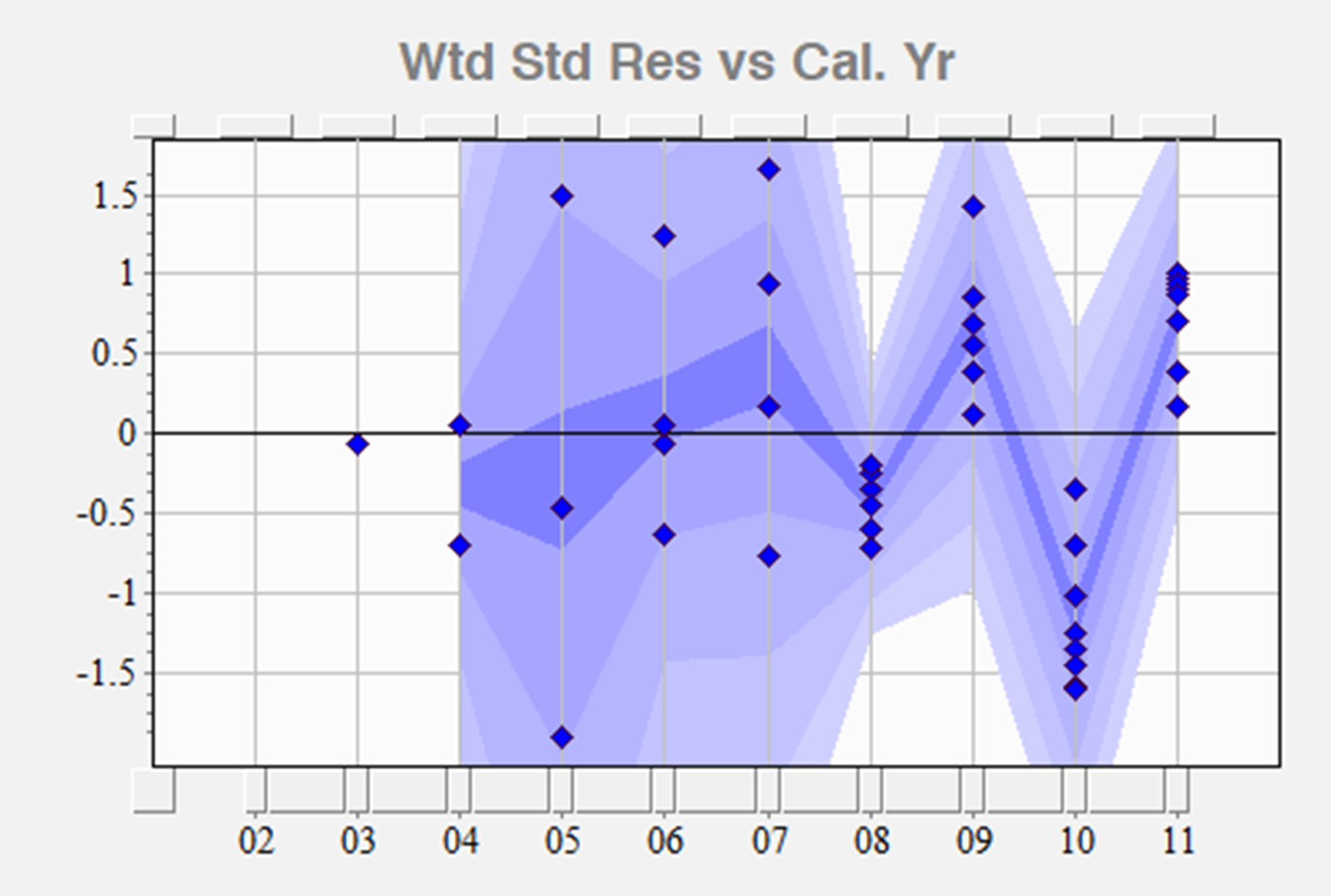

The display on the right shows a strong downward trend in the residuals (trend in data minus trend in method) versus calendar year.

This means a link ratio method, which cannot measure changing inflation trends, will grossly overstate the reserve estimates. The Mack method (volume weighted average) gives a total reserve of 902M. The arithmetic average link ratios gives a total reserve of 1.16B.

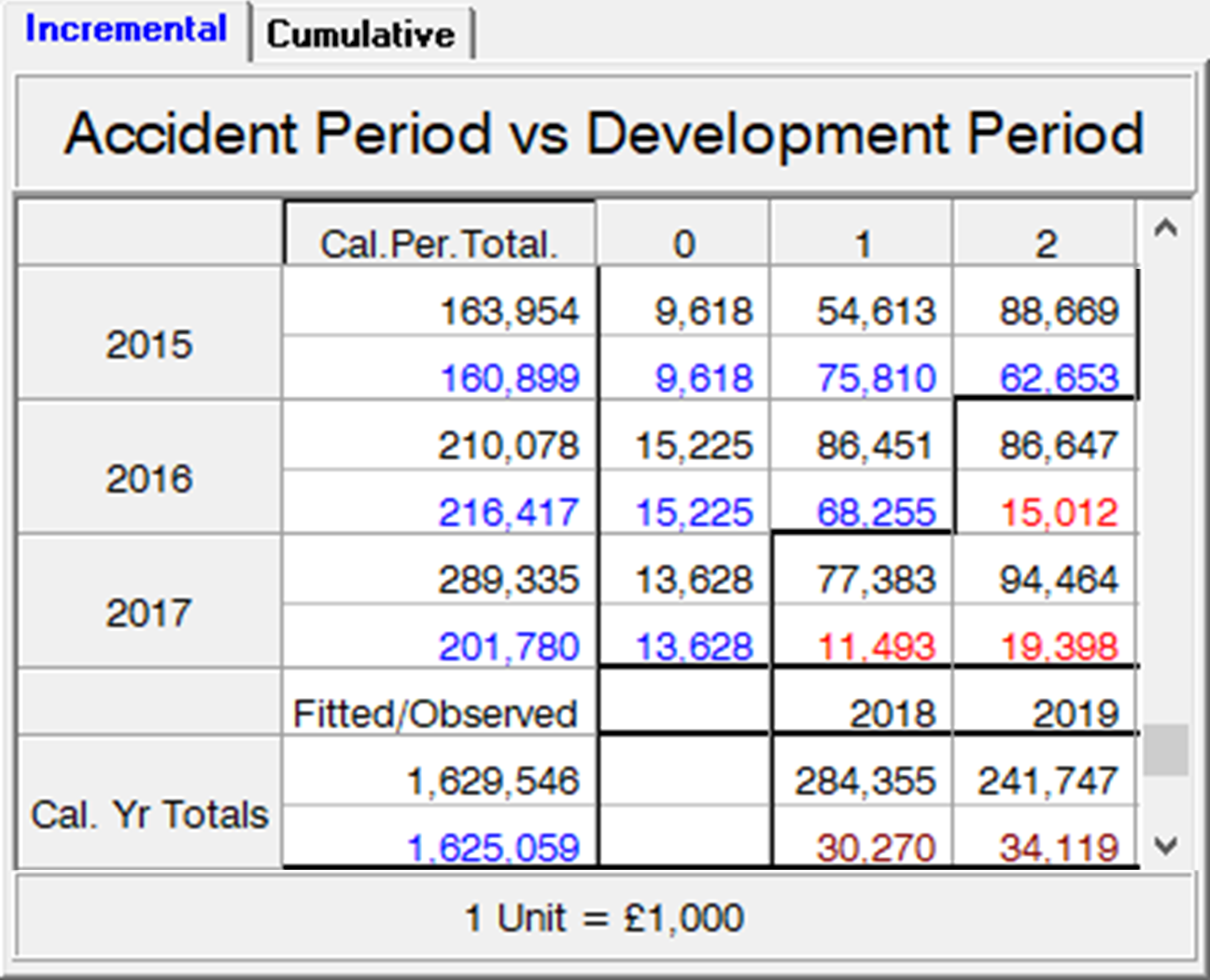

On the left is the forecast table (incremental version) for the Mack method.

The company just paid 202M GBP in 2017 (blue numbers are observed) but the fitted mean value (black numbers) is much higher at 289M. Further, the method is projecting the company will pay 284M GBP in the next calendar year!

The method clearly provides false indications.

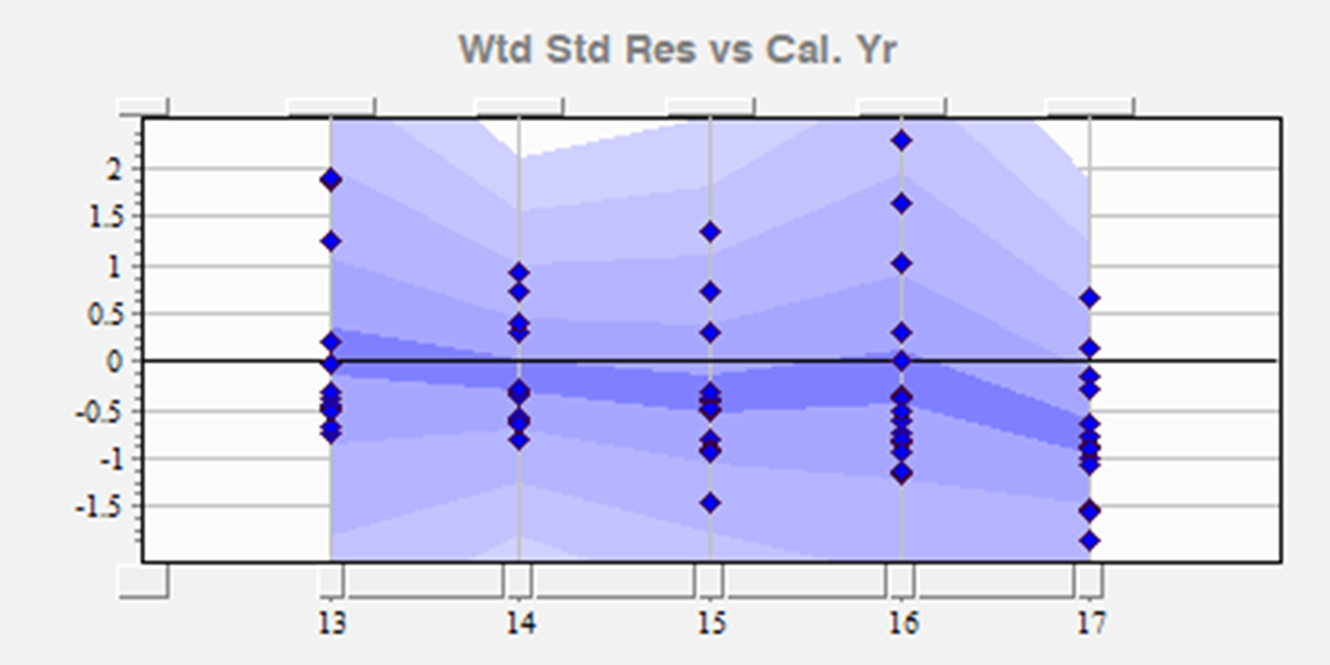

The optimal model identified in the Extended Link Ratio Family (ELRF) modeling framework applied to the last five calendar years has trends, intercepts, and very few ratios (because they have no predictive power). The residuals are much improved (left). The trends in the data are more in line with the trends in

the method.

The total reserve mean projected from this identified model is 504M – around half the original Mack method projected mean reserve! This is a much better estimate of the reserve mean, but how do we know it’s the best?

Let’s see what is really going on

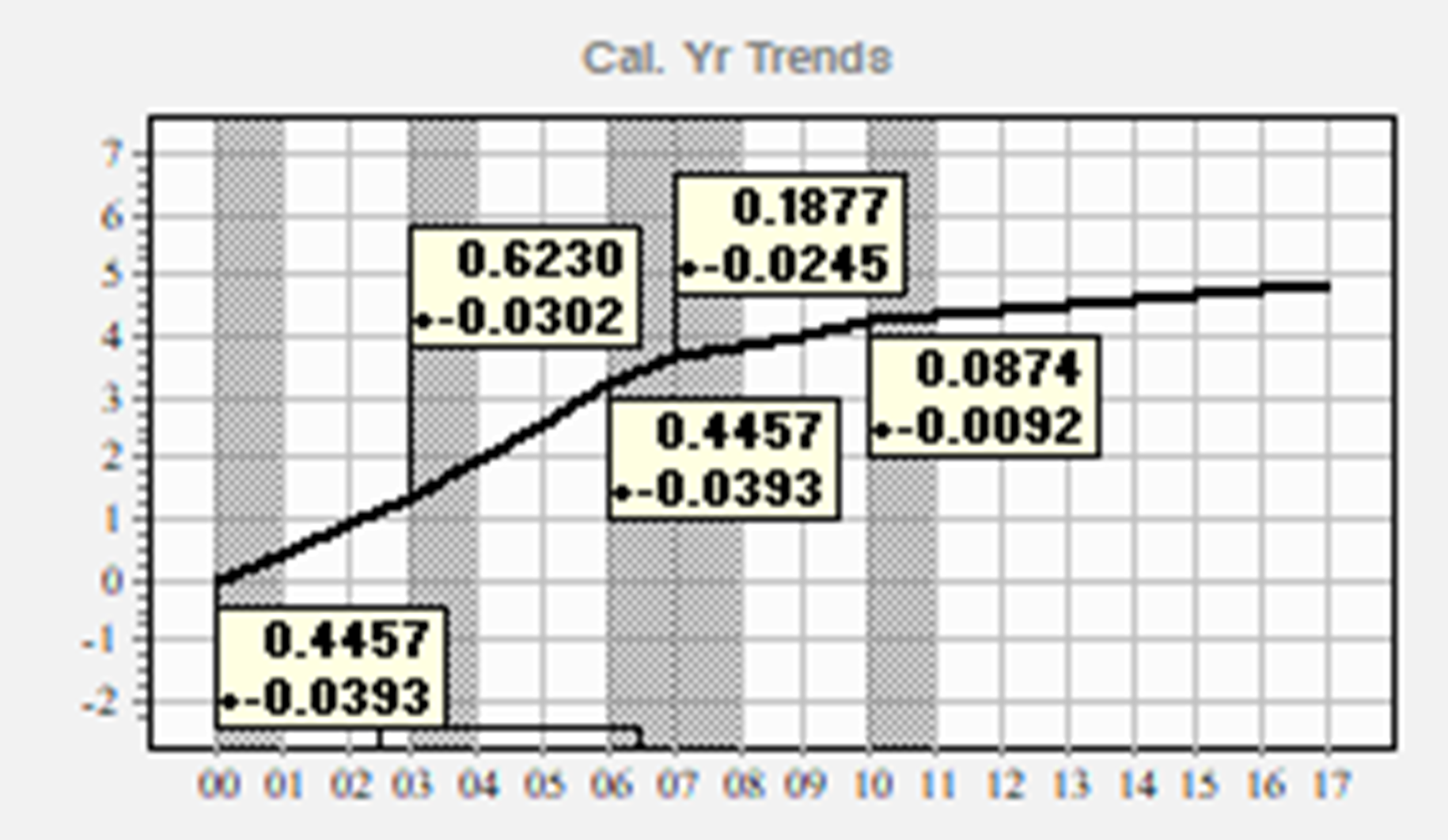

The identified model in the PTF modeling framework has calendar year trends as seen on the right. The calendar year trends are much lower more recently. Trends in other loss types (for instance: Case Reserve Estimates or Number of Claims Closed) can be related to the trends in the paid losses.

The actuary now has a narrative about the data.

Projections from the PTF model are much more realistic. The forecast scenario in PTF, using the 8.7%+_ calendar year trend, projects a mean payment of 223M GBP next year – much more in line with the recent history. The total mean reserve is 598M.

The actuary has control over all future trend assumptions in the PTF modeling framework. These can be related directly to the trends (or volatility) observed in the past – including CREs or NCC.

To get in the ballpark of the original forecasts of the Mack method, the future calendar year trend has to increase from the most recent 8.7%+_ calendar year trend to more than 25%+_ for the entire run-off period! If there are calendar period trends, especially calendar period trend changes then actuaries must have modeling frameworks which include the ability to parameterise these changes. Today, there are a plethora of inflationary features which are manifesting in P&C long tail lines - whether automobile insurance, worker's compensation, medical malpractice, or any other P&C LoB.

Incurred losses mask inflation in payments: projections too low

Maybe you think using Incurred Losses gives better estimates than Paid Losses?

Consider the Incurred Loss data from Best’s Schedule P (2011) for Tower Group.

On the right are residuals from the Mack method applied to the Incurred Losses. The zig-zag conflates the company's experience.

However, the key issue with modeling incurred data, is the inability to distinguish between payments amde and the case estimates.

If, for instance, the payments are trending up, and the case reserves are trending down - the underlying trends are masked when assessing the incurred losses.

For accuracy, it is always better to model the paid losses and case

reserves separately.

The total mean reserve projected by the Mack method is: 1.059B. The held reserves by the company as of 2011 were 921.9M. By calculating chain ladder ratios excluding the ‘high’ calendar years of 2009 and 2011, the forecasted total reserve drops to 950M.

The held reserves were supported by link ratio methods.

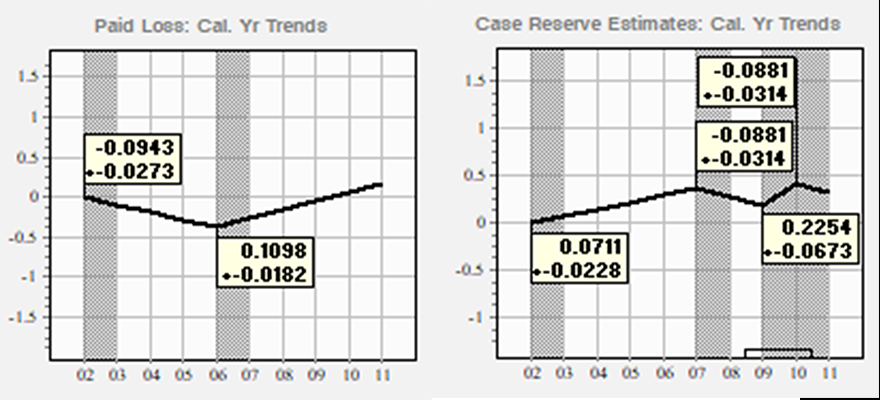

In the PTF modeling framework, Paid Losses and Case Reserves are modeled separately. Note the calendar year trends are not the same in the Paid Losses (left) and Case Reserves (right).

In order to reach the reserves held, the

calendar year trend for the future has to change from +11%+_ to -16.85%+_ - a total difference in trend of nearly 28%!!

This is impossible!

Without access to the PTF modeling framework, how would you know whether your projections are meaningful?

- Since 2006 the paid losses have been increasing 11%+_ faster than Earned Premium. This leads to an 11% increase in loss ratios (not reflected in the company’s held ultimates).

- Since 2007 the Case Reserve Estimates have been fluctuating (thus the masking of trends in the

Incurred Losses).

The forecast table on the left assumes the 11%+_ trend continues. The projections are increasing down the accident periods (eg: dev 4) just like the observed paid losses (blue numbers) in dev 0.

On the right is the forecast where the assumed future trend is set to -16.85%. Projected payments are decreasing down the accident periods (dev 4) despite the significant increases in observed paid losses and Earned Premium

(Tower Group went into administration in the fourth quarter 2013).

Social inflation higher more recently: projections averaging inflation too low

Consider anonymized Paid Loss data for a large Worker’s Comp provider.

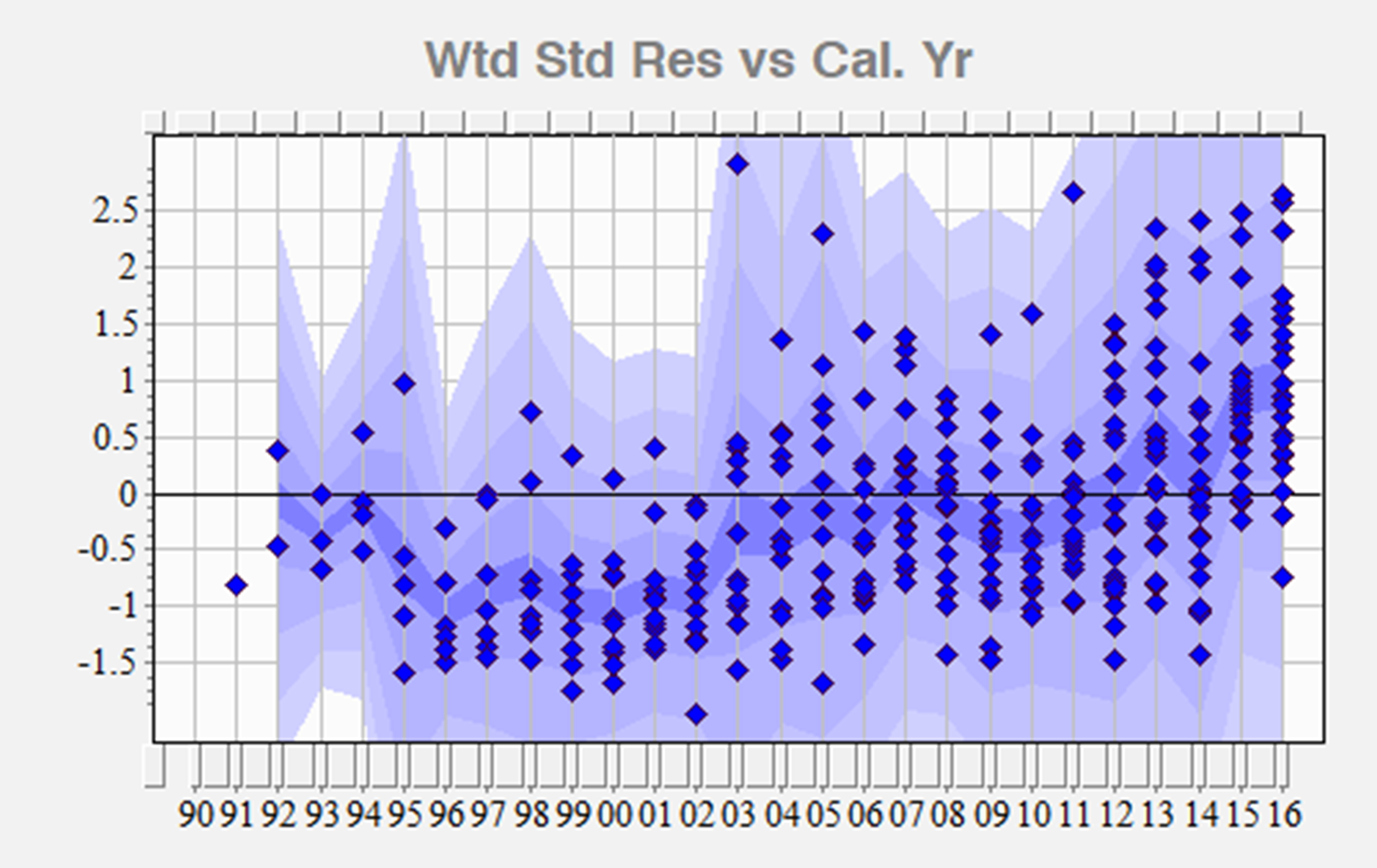

The display on the right shows a strong upward trend in the residuals (trend in data minus trend in method) versus

calendar year.

Any link ratio method will grossly understate the reserves – the trend in the method is less than the trend in the data. Using the Mack method (volume weighted average), the total reserve

is 839M.

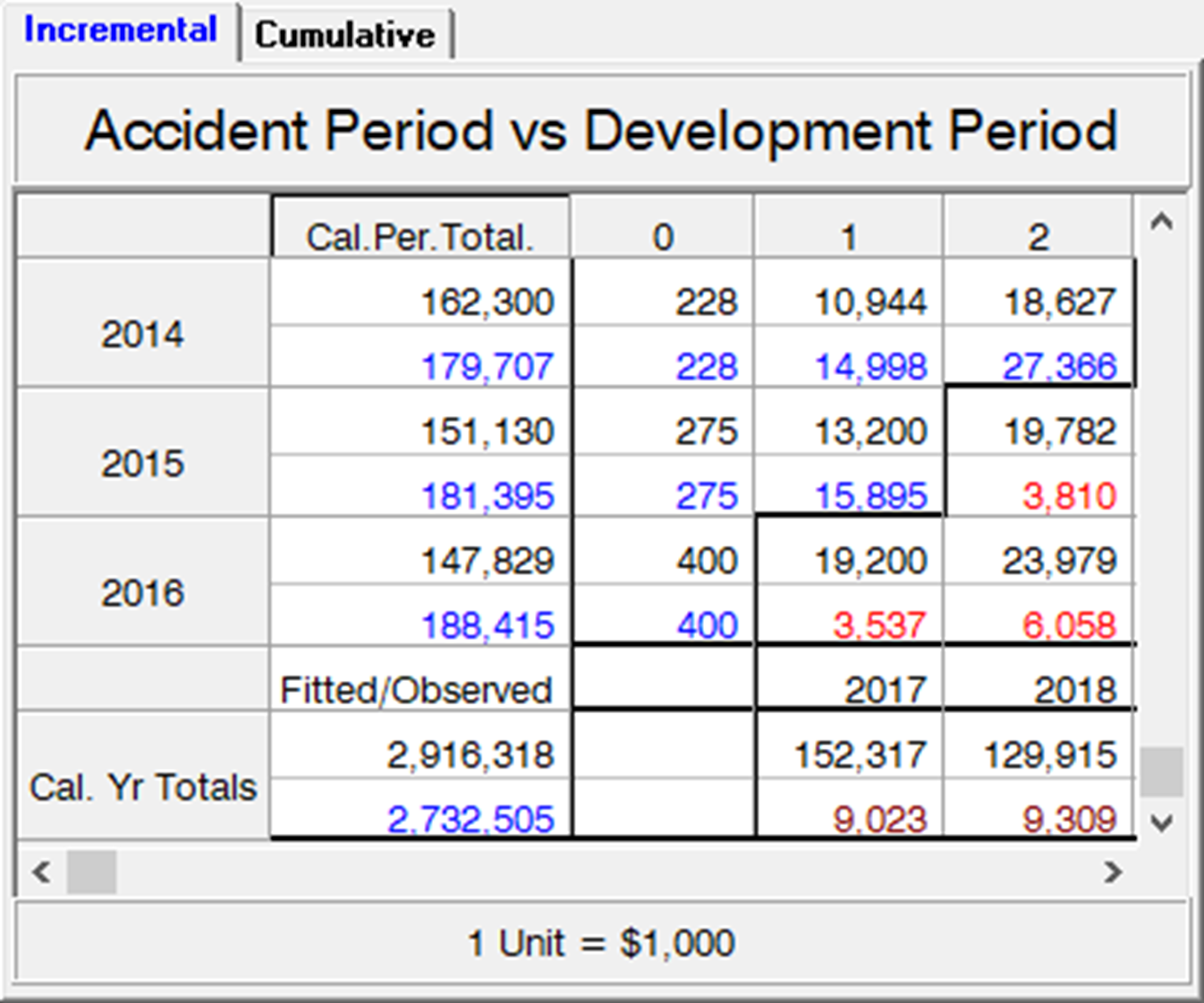

The company just paid 188M USD in 2016 (blue numbers are observed) and the method is projecting the company will pay 152M USD in the next calendar year (black numbers are

fitted means).

The method clearly provides false indications.

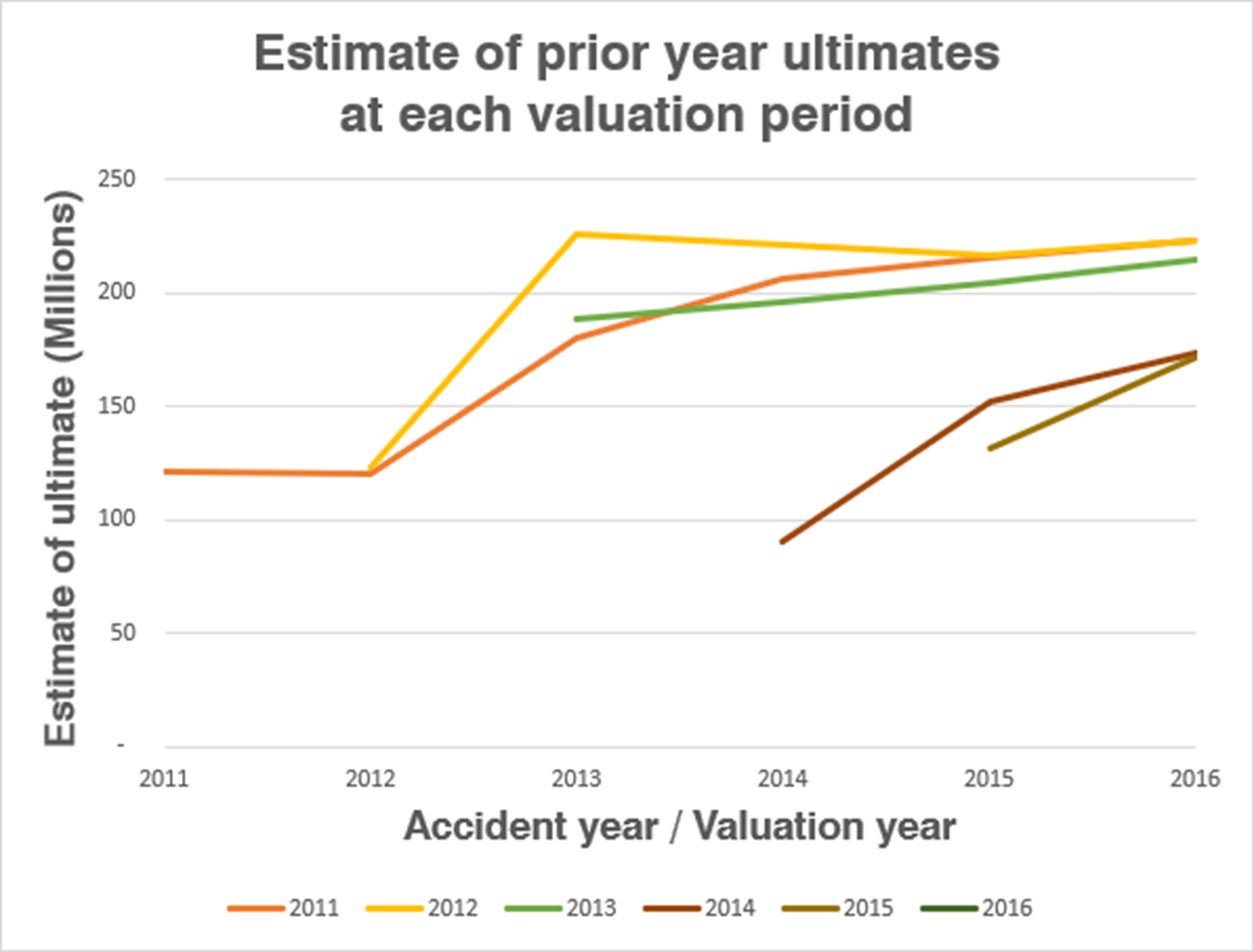

If every successive year you take weighted average link ratios of the last four years,each year the estimates of the prior year ultimates will increase, and projections of the paid losses for the next year will be too low.

To illustrate this, estimate the four year weighted average each valuation period from 2011 through to 2016 and plot the prior year ultimates.

Assuming the same link ratio method is applied in each of the four years, the company is in catch up mode.

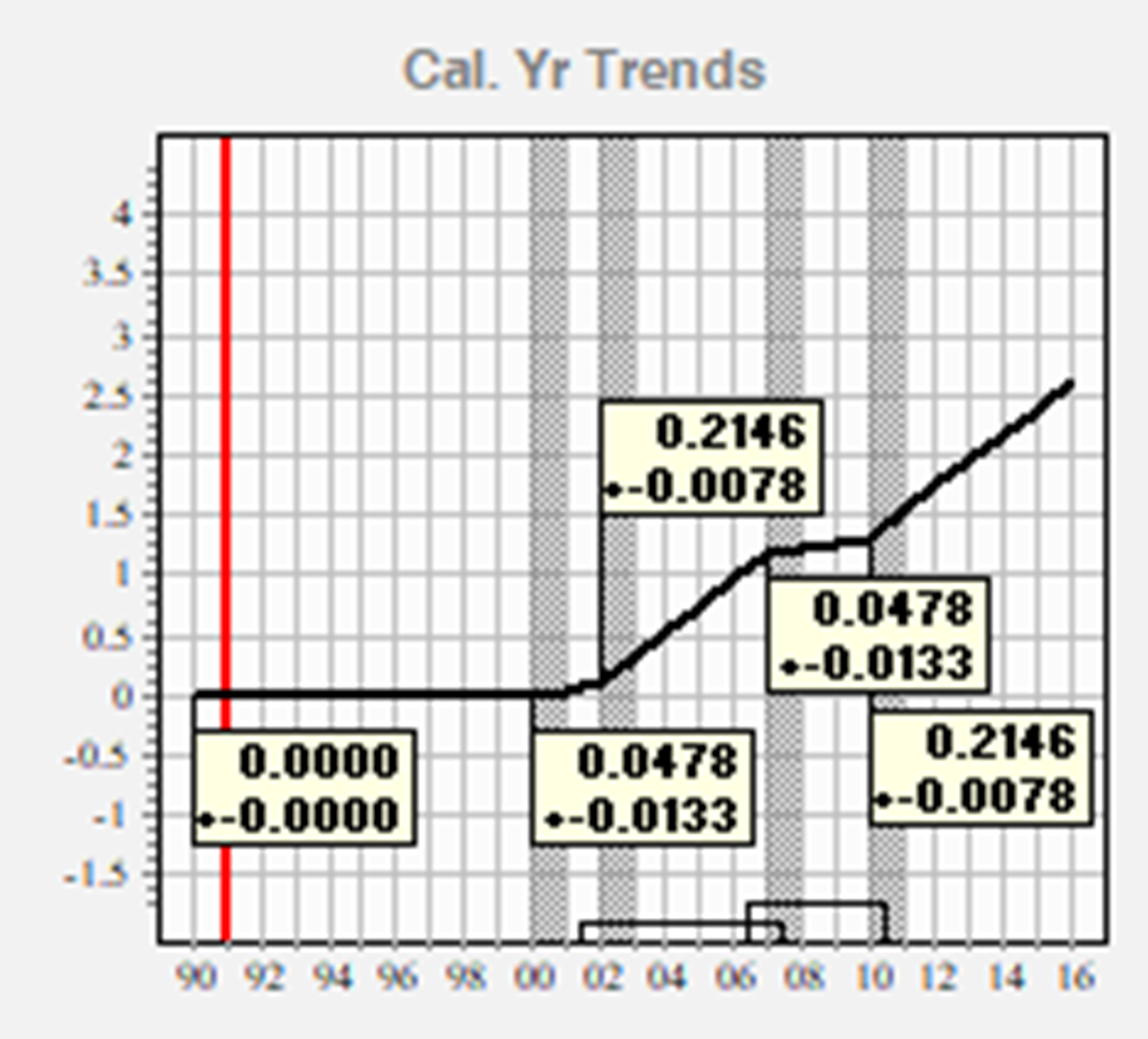

For this particular portfolio, the social inflation is very high.

The optimal PTF model, whose calendar year trends are displayed on the right, projects a total mean reserve of 1.309B if the trend of 21.46%+_ continues for several years.

Link ratio type methods cannot measure social inflation.

The PTF modeling framework enables you to mitigate model specification risk and extract maximum information from

the data.